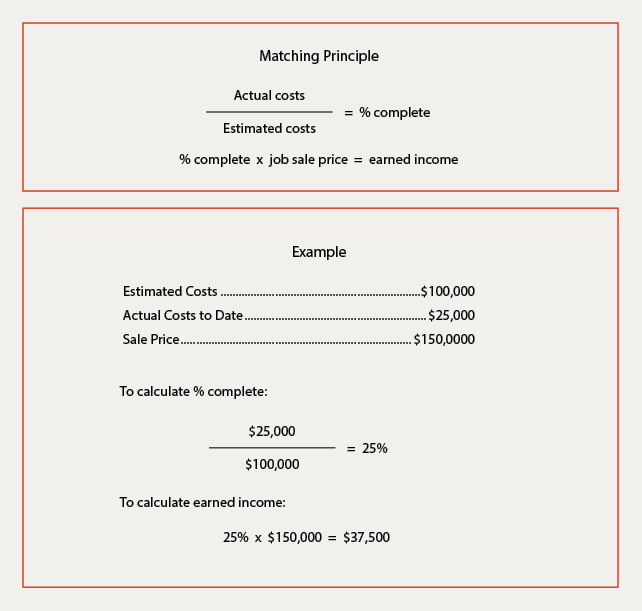

The matching principle is a common accounting concept that assumes a company will report expenses at the same time as the revenues they are related to. Revenues and expenses are “matched” on the income statement covering a period of time (typically, each month). The graphic above shows an example of how a company’s income would be calculated when the matching principle is applied:

Return to main article.